Today I “did a box” for the birdfeederAI and set it up to work in the garden. Within a couple hours it had detected and tweeted it’s first real life bird video! 🙂

Today I “did a box” for the birdfeederAI and set it up to work in the garden. Within a couple hours it had detected and tweeted it’s first real life bird video! 🙂

Found this beauty second hand (link). The kids and I had a lot of fun building and grabbing things with it. 🙂

Create a bird watching Artificial Intelligence that runs on a raspberry and tweets short videos every time it detects a bird. You can find mine at https://twitter.com/birdfeederAI

To build this bird watcher you will need the following hardware parts. Total cost EUR 255

mkdir -p /home/pi/dev/birdfeederAIcd /home/pi/dev/birdfeederAIpython3 -m venv ./venvsource ./venv/bin/activatewhich pythonwhich pipwhich pip3pip listpip install --upgrade pippip install opencv-python twython sudo apt install apt-filesudo apt-file updatefor i in find /home/pi/dev/birdfeederAI/venv/lib |grep so$|xargs ldd|grep "not found"|awk '{print $1;}'; do apt-file search $i|awk 'BEGIN{FS=":"};{print $1;}'; done|sort|uniq|xargs apt installcd /home/pi/dev/birdfeederAIgit clone https://github.com/chuanqi305/MobileNet-SSD.gitraspistill -o mypicture.jpgraspivid -t 5000 -o myvideo.h264

import cv2

cv2.namedWindow("TestCV2")

vc = cv2.VideoCapture(0)

if vc.isOpened():

rval,frame = vc.read()

else:

rval = False

while rval:

frame = cv2.flip(frame,-1)

cv2.imshow("TestCV2", frame)

rval, frame = vc.read()

key = cv2.waitKey(20)

if key ==27:

break

vc.release()

cv2.destroyWindow("TestCV2")

/home/pi/dev/birdfeederAI/auth.pycat>/home/pi/dev/birdfeederAI/auth.pyconsumer_key = 'puthereyourconsumerkey'consumer_secret = 'puthereyourconsumersecret'access_token = 'puthereyouraccesstoken'access_token_secret = 'puthereyouraccesstokensecret'Ctrl-Cgit clone https://github.com/Rogeman/birdfeederAI.git

import numpy as np

import cv2

import random

import os

import logging

from twython import Twython

from twython import TwythonError

from auth import (

consumer_key,

consumer_secret,

access_token,

access_token_secret

)

twitter = Twython(

consumer_key,

consumer_secret,

access_token,

access_token_secret

)

confidence_thr = 0.5

CLASSES = ["background", "aeroplane", "bicycle", "bird", "boat",

"bottle", "bus", "car", "cat", "chair", "cow", "diningtable",

"dog", "horse", "motorbike", "person", "pottedplant", "sheep",

"sofa", "train", "tvmonitor"]

COLORS = np.random.uniform(0, 255, size=(len(CLASSES), 3))

birdfeeder_dir=os.path.dirname(os.path.abspath(__file__))

logging.basicConfig(filename=birdfeeder_dir+'/log/birdfeederAI.log', level=logging.DEBUG, format='%(asctime)s %(message)s')

mobilenet_dir=birdfeeder_dir+'/MobileNet-SSD/'

net = cv2.dnn.readNetFromCaffe(mobilenet_dir+ 'deploy.prototxt' , mobilenet_dir+ 'mobilenet_iter_73000.caffemodel')

blob=None

def applySSD(image):

global blob

mybird = bool(False)

blob = cv2.dnn.blobFromImage(cv2.resize(image, (300, 300)), 0.007843, (300, 300), 127.5)

# pass the blob through the network and obtain the detections and

# predictions

net.setInput(blob)

detections = net.forward()

# loop over the detections

for i in np.arange(0, detections.shape[2]):

# extract the confidence (i.e., probability) associated with the

# prediction

confidence = detections[0, 0, i, 2]

if confidence > confidence_thr:

idx = int(detections[0,0,i,1])

if CLASSES[idx]=="bird":

mybird=bool(True)

return mybird

def birdRatio(videoName):

totalBirdFrames = 1

totalFrames = 1

vc2 = cv2.VideoCapture(videoName)

if vc2.isOpened():

rval2,frame2 = vc2.read()

else:

rval2 = False

while rval2:

birdinFrame = applySSD(frame2)

rval2, frame2 = vc2.read()

if (birdinFrame):

totalBirdFrames = totalBirdFrames + 1

totalFrames = totalFrames + 1

vc2.release()

return totalBirdFrames/totalFrames

videoLength=8*60*60*1000

randomsec=random.randint(0,videoLength)

#vc = cv2.VideoCapture(birdfeeder_dir+"/birds_video.mp4")

# If you want to record birds using your camera comment the above line and uncomment the below line. If you want to find birds in a video uncomment the line above and comment the line below 🙂

vc = cv2.VideoCapture(0)

vc.set(cv2.CAP_PROP_POS_MSEC, randomsec)

if vc.isOpened():

width = vc.get(cv2.CAP_PROP_FRAME_WIDTH)

height = vc.get(cv2.CAP_PROP_FRAME_HEIGHT)

fps = vc.get(cv2.CAP_PROP_FPS)

fcount = vc.get(cv2.CAP_PROP_FRAME_COUNT)

else:

logging.error('Can\'t open video')

exit()

recording= False

framerecorded = 0

framecounter = 0

birdinFrame=False

fourcc = cv2.VideoWriter_fourcc(*'h264')

#out = cv2.VideoWriter('output.mp4',fourcc,20.0,(640,480))

out = cv2.VideoWriter(birdfeeder_dir+'/output.mp4',fourcc,fps,(int(width),int(height)))

if vc.isOpened(): # try to get the first frame

rval, frame = vc.read()

(h, w) = frame.shape[0] , frame.shape[1]

else:

rval = False

logging.debug('Started main loop')

while rval:

#You enter this loop once per frame

rval, frame = vc.read()

#uncomment the below line if you need to flip the camera upside down.

frame = cv2.flip(frame,-1)

key = cv2.waitKey(20)

if key == 27: # exit on ESC

break

framecounter = framecounter + 1

if (framecounter > 60):

# Write frame to disk every 60 frames so we can see what the camera is seeing

framecounter = 0

cv2.imwrite(birdfeeder_dir+"/webserver/currentframe.jpg",frame)

if (birdinFrame==False):

#Check if this frame has a bird in it

birdinFrame= applySSD(frame)

if (birdinFrame== True and recording== False):

#You have detected the first bird in a frame, start recording

logging.info('Started recording video')

recording=True

if (recording == True):

#write the frame to file keep track of how many frames you have saved.

framerecorded = framerecorded + 1

out.write(frame)

if (framerecorded > 200):

#after 200 frames stop recording

logging.info('Checking recorded video')

recording = False

birdinFrame=False

framerecorded = 0

out.release()

filename = birdfeeder_dir+"/output.mp4"

birdsinvideo= birdRatio(filename)

logging.debug('percentage of bird in video: '+birdsinvideo)

if (birdsinvideo> 0.50):

# if the recorded video has more than 50% of frames with a bird in it then tweet it

logging.info('Tweeting bird video')

video = open(filename,'rb')

try:

response = twitter.upload_video(media=video, media_type='video/mp4', media_category='tweet_video', check_progress=True)

twitter.update_status(status='birdfeeder 0.5', media_ids=[response['media_id']])

except TwythonError as e:

logging.error('Twitter error:'+str(e))

birdsinvideo=0

video.close()

randomsec=random.randint(0,videoLength)

vc.set(cv2.CAP_PROP_POS_MSEC, randomsec)

os.remove(birdfeeder_dir+'/output.mp4')

out = cv2.VideoWriter(birdfeeder_dir+'/output.mp4',fourcc,fps,(int(width),int(height)))

vc.release()

sudo apt-get update && sudo apt-get upgrade

curl -fsSL https://get.docker.com -o get-docker.sh

sudo sh get-docker.sh

sudo usermod -aG docker pi

sudo reboot

docker run -it --rm -d -p 8080:80 --name web -v /home/pi/dev/birdfeederAI/webserver/:/usr/share/nginx/html nginx

cat > /home/pi/dev/birdfeederAI/webserver/index.html

<html>

<head>

<title>Birdfeeder</title>

<meta http-equiv="refresh" content="2" />

</head>

<body>

<img src=./currentframe.jpg>

</body>

</html>

Ctrl+C

You can now open a web browser to your raspberry pi’s ip address port 8080 and see what your camera is seeing

We add birdfeeder to systemd so it starts on boot.

vim /home/pi/dev/birdfeederAI/bin/birdfeeder.shchmod +x /home/pi/dev/birdfeederAI/bin/birdfeeder.sh

#!/bin/bash

docker run -it --rm -d -p 8080:80 --name web -v /home/pi/dev/birdfeederAI/webserver/:/usr/share/nginx/html nginx

source /home/pi/dev/birdfeederAI/venv/bin/activate

while [ 1 -eq 1 ]

do

nice python /home/pi/dev/birdfeederAI/birdfeeder.py

done

sudo vim /lib/systemd/system/birdfeeder.service

[Unit]

Description=birdfeeder service

After=multi-user.target

[Service]

Type=idle

ExecStart=/home/pi/dev/birdfeederAI/bin/birdfeeder.sh

[Install]

WantedBy=multi-user.target

sudo chmod 644 /lib/systemd/system/birdfeeder.servicesudo systemctl daemon-reloadsudo systemctl enable birdfeeder.servicesudo rebootI enjoy tinkering around with robots and electronics. Bridging the invisible world of software with the real world of physical things.

I discovered I could glue a breadboard to the side of the base of this robotic arm, and that I could hold the arduino board to the base with elastic bands. and that the adafruit motor board left 5 analog pins free to use, and that I could put a switch, a potentiometer and an hbridge in the breadboard with these five free pins. And that I could substitute the broken led with a new one with my soldering iron 😀

It is now all ready and working. Every time I hold down the switch button it activates one of the five motors iteratively. With the potentiometer I can have the motor run in one direction or the other. And the LED at the hand of the robot arm shines while the button is pressed.

The only problem pending is I need to change all the worn out gears from the motors as they are eroded from previous experiments (the problem with dc motors as opposed to servo motors is that you can’t know where they are, so I overextended them eroding the gears)

I started self-training on machine learning. I bought a copy of “Hands-On Machine Learning with Scikit-Learn, Keras & Tensorflow” and am enjoying it a lot. I have a small moleskine with which I break down the concepts one day at a time 🙂

So far I have not yet encountered any concept which is not trivial. This means I am progressing. In my experience things are either trivial or impossible. Our job is to break down impossible tasks until they become trivial 🙂

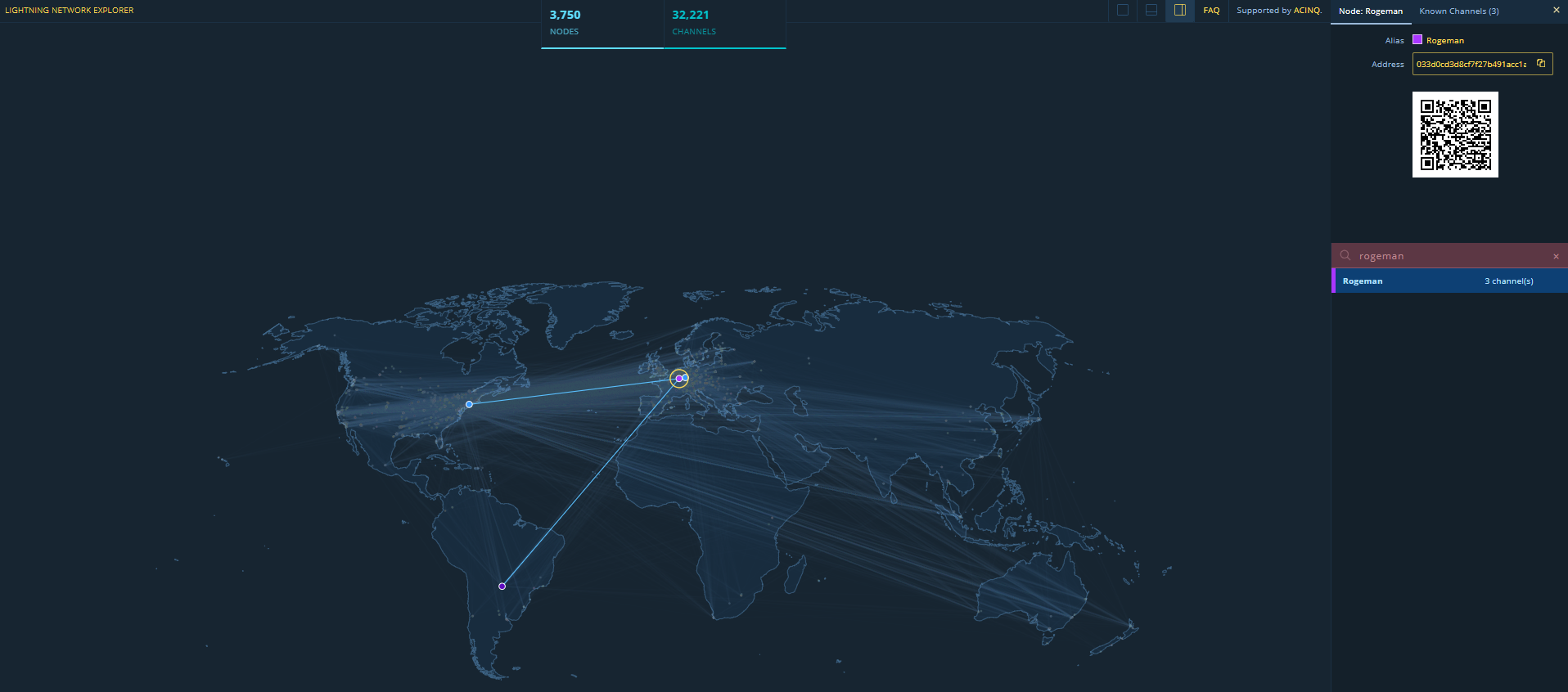

Now that you have your node set up and you have established a few channels you can start routing payments. You can see my node here I have opened three channels for now, and with it I am able to route payments anywhere.

You can set up a tippin.me account to receive tips in satoshis. It creates a custodial lighning wallet where people can send you tips. You can send me some satoshis at https://tippin.me/@Rogeman (as of today 1 satoshi equals 0.00003416 Euros, so don’t be shy, if you go wild and send 1,000 satoshis it will be 3 cents of a euro 😉 )

To send a tip to tippin.me you need to use the payinvoice command, instead of the sendpayment command as you won’t have an invoice and you can send any amount you want.

lncli --lnddir /opt/lnd-data/ --no-macaroons payinvoice --pay_req lnbc1pw8aa5app5t3zqgnsq2e80s47s33a4rqc4w3spvamwp5tch732zucgglcyefwqdph235hqurfdcs9ymm8v4kkzm3q9p6xjursd9hzumt99y582vfj8ycny2gcqzysxqyz5vqu05rc3mk3m5cteh8gsvh3pf696p4wfdeezq29kkxcdrwjmtj64njk5lj4nv4jul96jcsqvw94a57y4722lrzdygu87jfkw2leu9ceqqpqmmcgl --amt 100On the testnet a very cool test to do is buy a Blockaccino at starbloqs, check out a video here

You can request others to send you money by sending them an invoice

lncli --lnddir /opt/lnd-data/ --no-macaroons addinvoice 100 --expiry 36000

{

"r_hash": "f9ba7fd5b0be3d768c29aa951b4a215ea7e37133ebb41fd5a7d424e7981551de",

"pay_req": "lnbc1u1pw8a7u6pp5lxa8l4dshc7hdrpf4223kj3pt6n7xufnaw6pl4d86sjw0xq4280qdqqcqzysxqypr9qfrglxdwv8jdc9xlsyatugwztdvsn89y4hmlm2mgds5wyl9k3c963uk66zhntp6940yxpfz5fa0au9mcg4c0sfc77eg589fmpnjhcs6gp49ghuh",

"add_index": 1

}Once you’ve created the invoice you can send the pay_req to the payer (in the above example lnbc1u1pw8a7u6pp5lxa8l4dshc7hdrpf4223kj3pt6n7xufnaw6pl4d86sjw0xq4280qdqqcqzysxqypr9qfrglxdwv8jdc9xlsyatugwztdvsn89y4hmlm2mgds5wyl9k3c963uk66zhntp6940yxpfz5fa0au9mcg4c0sfc77eg589fmpnjhcs6gp49ghuh)

Others can send you money with the sendpayment command by paying your invoice

lncli --lnddir /opt/lnd-data/ --no-macaroons sendpayment --pay_req=nbc1u1pw8a7u6pp5lxa8l4dshc7hdrpf4223kj3pt6n7xufnaw6pl4d86sjw0xq4280qdqqcqzysxqypr9qfrglxdwv8jdc9xlsyatugwztdvsn89y4hmlm2mgds5wyl9k3c963uk66zhntp6940yxpfz5fa0au9mcg4c0sfc77eg589fmpnjhcs6gp49ghuhWith your lightning network node you can send payments which are:

One problem lightning network has is that you can only send or receive as much money as you have route bandwidth for, this means that if you want to be able to receive payments worth 500 Euro, you need to have channels open worth 500 Euro. This can be pretty expensive for high value payments. Due to this constraint the lightning network can work very well for low value payments, like buying a coffee, and not so well for high value payments like buying a house. In any case high value payments can be done directly using the bitcoin blockchain without using the lightning network layer and are usually not done in high volumes. (Maybe a third layer protocol could be used to spit large payments into groups of smaller ones similarly how tcp over ip is capable of splitting large packets of information into smaller ones and guarantee order and completeness, you could split a payment of 1000 satoshis into two payments of 500)

This is the future of how robots will pay each other.

Lightning network is a Layer 2 protocol that sits on top of the bitcoin/litecoin blockchain. It enables instant, low cost, anonymous payments by routing payments through point to point channels in a similar way to what the correspondent banking system uses today to transfer fiat currency.

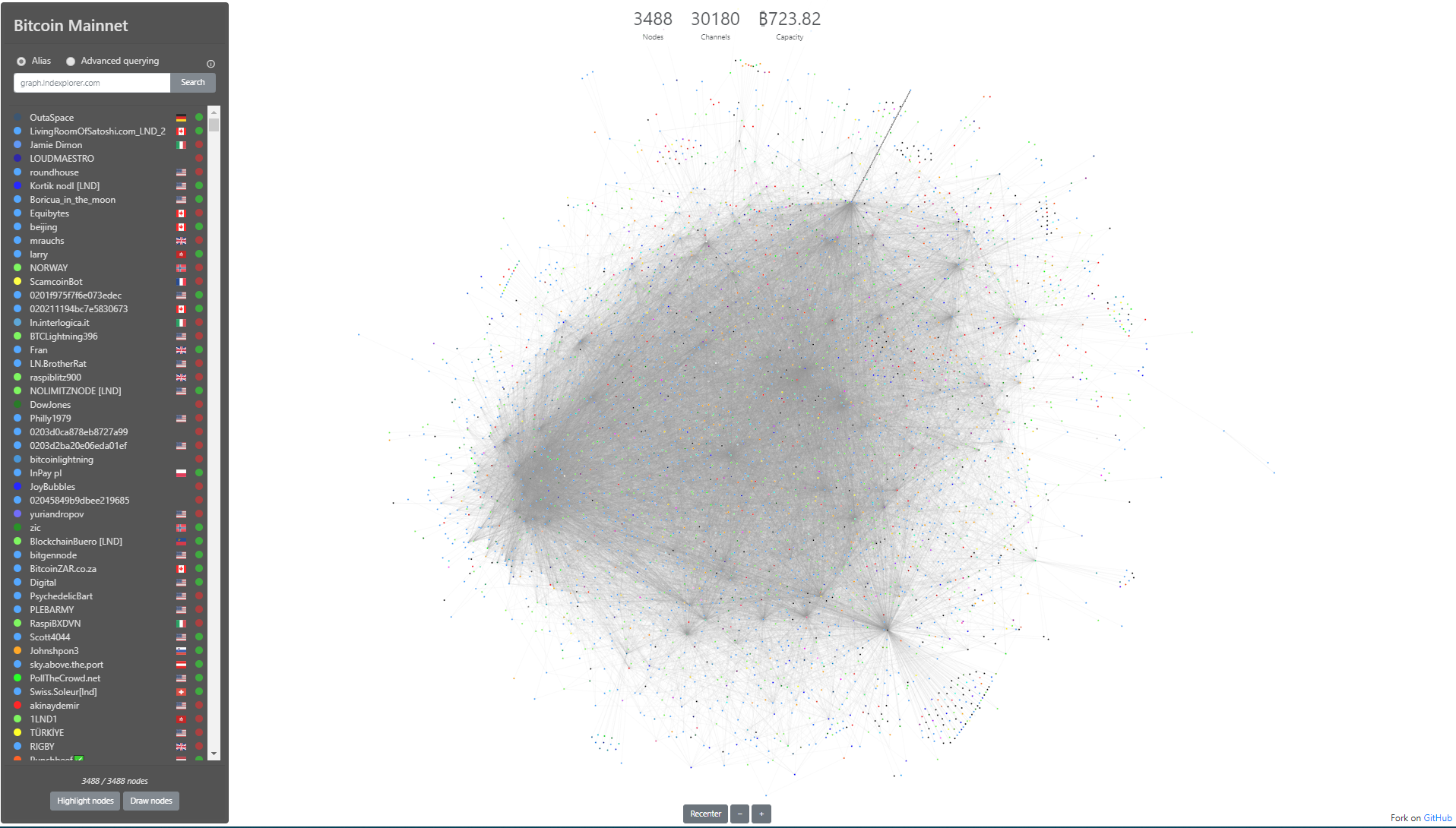

You can check out the map of channels of the lightning network at https://graph.lndexplorer.com/ as of today, there are 3488 nodes

In order to set up your lightning network node, first you need to set up your bitcoin node. Here you have simple instructions to set it up by compiling it from source.

First we clone the git repository for the bitcoin core node

sudo apt-get install git

mkdir $HOME/src

cd $HOME/src

git clone https://github.com/bitcoin/bitcoin.gityou will need libzmq3 in order for the lighning node to communicate with your bitcoin node, so we need to install libzmq3-dev

sudo apt install libzmq3-devnow we configure and install the node

cd bitcoin

./autogen.sh

./configure

make

sudo make installbitcoind is installed! 🙂 now we need to create a config file and create an rpc user and password so you can communicate with your bicoind node

./share/rpcauth/rpcauth.py roge

#This command will give you the user and password you will need to include in your bitcoin.conf

String to be appended to bitcoin.conf:

rpcauth=roge:793845a197311a324722f93e8360e166$3dfb9011930a6fcb85c99e0e1ad2e0309958b2aa863955faae831e0eeec3894f

Your password:

34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A=Let’s create a directory where all bitcoin data will be stored. Be warned that this directory will hold a copy of the whole bitcoin blockchain which is as of today 243 GB.

We will copy a bitcoin.conf file to the bitcoin data folder

mkdir /opt/bitcoin-data/

cp $HOME/src/bitcoin/share/examples/bitcoin.conf /opt/bitcoin-data/now we edit the bitcoin.conf file, the following variables are important

vi /opt/bitcoin-data/bitcoin.conf

#set testnet to 1 if you'd like to run a node for testing purposes not using real bitcoins.

testnet=1

#set daemon=1 to launch bitcoind as a daemon running in the background

daemon=1

#set rpcauth to the rpcuser you created earlier

rpcauth=roge:793845a197311a324722f93e8360e166$3dfb9011930a6fcb85c99e0e1ad2e0309958b2aa863955faae831e0eeec3894fWe are set. Now we can start our bitcoind node with the following command. It could take one or two days to synchronise with the bitcoin blockchain.

bitcoind --datadir=/opt/bitcoin-data/ -rpcuser=roge -rpcpassword=34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A=you can monitor progress looking at debug.log

tail -333f /opt/bitcoin-data/debug.logyou can connect to your bitcoind node using bitcoin-cli which allows you to manage your node

watch bitcoin-cli -datadir=/opt/bitcoin-data/ -rpcuser=roge -rpcpassword=34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A= getblockchaininfoNow encrypt your wallet don’t forget this password. Write it down on a piece of paper and store that paper somewhere safe.

bitcoin-cli -datadir=/opt/bitcoin-data -rpcuser=roge -rpcpassword=34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A= -stdin encryptwallet

writehereyoursupersecretpassword

Ctrl-dnow you can get an address where to deposit bitcoin in (you can buy these bitcoins in exchange for fiat currencies such as Euros or Dollars in exchanges like kraken.com or blockchain.org) do not send real bitcoin to a testnet wallet, they will be lost. You can get free testnet bitcoins by googling testnet bitcoin faucet. Here’s one (link)

bitcoin-cli -datadir=/opt/bitcoin-data -rpcuser=roge -rpcpassword=34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A= getnewaddress

#This will return the new address where you can send bitcoin to

# the command will return something like 3NUvF2fvitxrU1fY43rCQivx9RtCgvXuEbOnce you have transferred bitcoins to your wallet you can see your balance

bitcoin-cli -datadir=/opt/bitcoin-data -rpcuser=roge -rpcpassword=34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A= getbalance

#This command will output your bitcoin balance

0.00001In order to transfer bitcoins to another address you first need to unlock your wallet for x seconds

bitcoin-cli -datadir=/opt/bitcoin-data -rpcuser=roge -rpcpassword=34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A= -stdinn walletpassphrase

enteryoursupersecretpassword

enternumberofsecondsthatthewalletwillremainunlocked

Ctld-dNow you can transfer bitcoin to another wallet

bitcoin-cli -datadir=/opt/bitcoin-data -rpcuser=roge -rpcpassword=34ZofsEbG95rWITDv8w03crrzIYBioGAKfMqDq1yY1A= sendtoaddress enterthedestinationaddress entertheamounttotransferYou can find all the bitcoin-cli commands here: https://en.bitcoin.it/wiki/Original_Bitcoin_client/API_calls_list

Now that our bitcoin node is ready, let’s set up our lightning network node! 🙂

One of the funnest games I’ve played this year. Awesome Music, graphics, and playability. I’ve enjoyed it a lot! 😀

MongoDB is a nosql database. This means that you don’t use SQL to query the data, instead you use javascript and receive responses in json objects. I enrolled in course M001: Mongodb basics to get a basic understanding of how it works and it seems extremely easy.

The cool part about it being javascript based is that you can become a “full stack” web developer just by learning javascript. The front end with angular, and the backend with node.js and mongodb can be sufficient for you to build web apps. (I still shudder thinking that javascript is being used for anything, yet here we are..)

Mongodb is extremely easy to start playing with, for free you can create a database cluster in the cloud with 512MB by registering in mongodb.com and getting a Mongodb atlas.

MongoDB Compass is a graphical client with which you can connect to your database and analyse your data. It analyses the data and gives you insights on the types of data, you can also filter just by selecting with your mouse the data you want to filter on in an intuitive way.

The CLI is the best way to power-query your data. below my cheat-sheet after completing the basic training course:

MongoDB cheatsheet

Another year, another euskalencounter.org 🙂 This year I’ve binge watched Altered Carbon, and katakoda’s Docker training, below is my cheat sheet for future reference.