Fintech is short for “Financial Technology” and covers all technologies applied to finance. It is used mainly to refer to disruptive innovations in the Financial industry which is a topic that’s getting a lot of traction, specially since in 2008 Satoshi Nakamoto published his 9 page paper on bitcoin. However, many of these fintech disruptions don’t necessarily come from new technologies, just new ways of using existing technology.

One way fintech disruption can be classified is

- Infrastructure: Technical Innovations to infrastructure are necessary to solve business problems and enable disruption.

- Identity: One of the big concerns of regulators is KYC (Know your customer). In an online world, what can be done to ensure that a person is who he claims to be? With the concept of wallets which are anonymous, what can be done to ensure money movements can be associated with their owners? This is important to avoid money laundering, financing of terrorism, tax evasion…

- Privacy: On the other end of the spectrum of KYC, privacy is also important for end users. MIT are working on Enigma which is a blockchain based, distributed computer similar to Ethereum but with a focus on solving the millionaire’s problem (two millionaires want to know who of them is richer without disclosing their wealth) and allow calculations to be performed by the nodes without disclosing the data (but only pieces of the data which do not give a vision regarding the whole)

- Security: If all my bitcoins are sitting in my bitcoin wallet, which is a file in my computer and I lose my file, or forget my password, all my bitcoins are gone forever. If a hacker was able to copy my wallet, which is just a normal file, and was able to find out my password (for example hacking my keepass by compromising my computer) he could transfer all my bitcoins to his wallet and I would have lost them forever.

- Money and Payments: Mankind has come a long way from the cash only world where currency was backed by precious metals. Plastic credit and debit cards are the current norm. Paypal, near touch payments with mobile devices are trying to become mainstream, but a big disrupting technology has emerged in 2008: The Blockchain. The Blockchain enables:

- peer to peer payments:

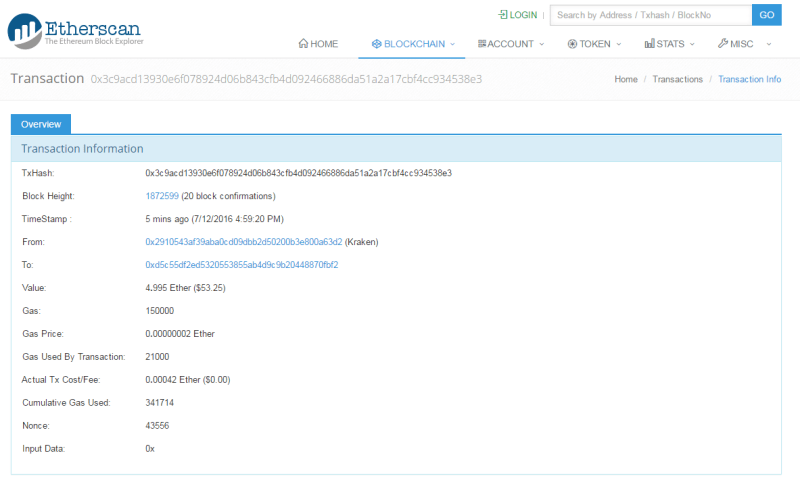

- Until now when Alice wanted to send Bob money remotely, the only way to do this was to go through a trusted intermediary (a bank, a remittance company, paypal…). With blockchains like the one used by Bitcoin or Ethereum Alice can pay Bob directly, with no intermediary, and more importantly almost no fees. This will radically improve the lives of people who try to send money back to their families in developed countries, for which they need to pay exorbitant fees, wait in line and hope that the money is not lost, while at the other end of the transaction, the recipient has to go through a similarly daunting process.

- The peers in a transaction don’t neccesarily need to be human. M2M (Machine to machine) payments is something that can be feasible. For example slock.it is building locks that will open if a smart contract tells them to open.

- Cryptographically guarantee that a record can not be modified

- Entries in the blockchain cannot be modified. The older an entry is the more time it would take an attacker to be able to forge an alternative chain. Thanks to proof of work, we can rest assured that an attack is not possible. I’ll go deeper into these fun techie ideas in future posts.

- smart contracts

- Smart contracts enable programs to be run on the blockchain allowing these programs to send payments automatically if certain conditions are met (for example Alice could bet with Bob on the outcome of a match. The smart contract could check for the result of the match and transfer the money from Alice to Bob automatically once the result is known)

- immediate settlement

- Currently in capital markets, settlement is done two or three days after the trade is done due to the complex legacy infrastructure that it must go through. With blockchain, the transaction could be settled in minutes instead of days.

- No settlement risk

- Since transactions are atomic, the transaction either gets done or it does not. Hence there would be no settlement risk. However there are some views that claim that a blockchain can never really finalise a transaction as it is theoretically possible that due to the way the consensus algorithm works, the latest blocks may be rolled back. Vitalik Buterin, founder of the Ethereum foundation argues that by that same logic, the current system can also never really finalise a settlement, since the registry could be burnt down or defaced by a malicious user.

- peer to peer payments:

- Capital Markets:

- In the capital markets space, disruptive technologies are emerging in the form of:

- Robo-Advisors: Artificial Intelligence is enabling automated investment advice. For example Betterment.com, Robinhood.com or Wealthfront.com offer this service

- Equity crowdfunding: A trend towards equity crowdfunding is emerging where shares in the company would be acquired by the crowdfunders, an example of this is Fundersclub.com or equitynet.com

- Blockchain driven markets: Digital Asset Holdings is a very strong startup, aiming at creating a market which is settled over a blockchain. Many strong incumbents are backing this initiative which looks very promising. This platform would deliver on the promise of instant settlement. Ethereum and Digital Asset Holdings are the two fintech disruptors which interest me the most.

- In the capital markets space, disruptive technologies are emerging in the form of:

- Marketplaces:

- SME lending companies such as Bond Street, On Deck, or Funding Circle are enabling investors to fund SMEs without SMEs needing to ask a bank

- Banking the unbanked: Mpesa is a vodafone initiative which allows people in developing countries to send and receive money from their cellphones via PIN protected SMS. Users can recharge their accounts through airtime resellers and retail outlets playing the role of banking agents.

- Credit ratings for the unbanked: companies like First Access are allowing individuals and SME in developing countries to obtain a credit rating when applying for a loan at a bank. First Access gain permission from the client to acquire his cellphone payment history from his cellphone provider, with this history of payments they can give the bank a credit rating for a direct loan.